There are a lot of positive things about getting married, but the IRS' marriage penalty isn't one of them. The marriage penalty occurs when you pay more tax as a married couple than you would as two single filers making the same amount of money. It pops up again and again in the federal tax code. The Tax Rate ProblemAfter two people are joined in matrimony, you may think the income levels for their tax brackets would simply be double what they were when they were single. But that's not the case: instead, the thresholds to move into a higher tax bracket are lower for married couples. Example: As a single filer, Mr. Smith's $90,000 income has a top tax rate of 25 percent, the same as his bride-to-be's tax rate on her $75,000 income. Once they're married, their combined income of $165,000 moves their top income tax rate to 28 percent. In this case, being married exposes some of their income to an extra 3 percent tax versus staying single. Accelerating Phase-OutsMarried couples also see personal exemptions and itemized deductions phase out faster than for single filers. These deductions begin to phase out when adjusted gross income is greater than $261,500 for single filers, but only $313,800 (versus an expected amount of $523,000) if you’re married filing a joint return. These tax benefit phase-outs don't just affect upper-income taxpayers. Even the earned income tax credit (EITC) phase-outs favor single over married taxpayers. A single mother of three can qualify for the EITC with income less than $48,340, while a married couple loses the EITC with combined income over $53,930. In this way, a married couple with $27,000 in income each are severely penalized when using the EITC when compared with staying single. ACA Piles onto the Marriage PenaltyThe Affordable Care Act (also known as "Obamacare") also penalizes married couples with lower thresholds on its 0.9 percent wage surtax and 3.8 percent investment income tax. The income thresholds for these surtaxes are $200,000 for single filers and $250,000 for married couples filing jointly. As a result, singles who each earn $125,000 to $200,000 can get hit with the extra tax after they marry.

Unfortunately, there are some couples who simply decide not to marry to avoid the marriage penalty. If you are planning to marry in the near future, don't be caught by surprise with a larger than expected tax bill.

0 Comments

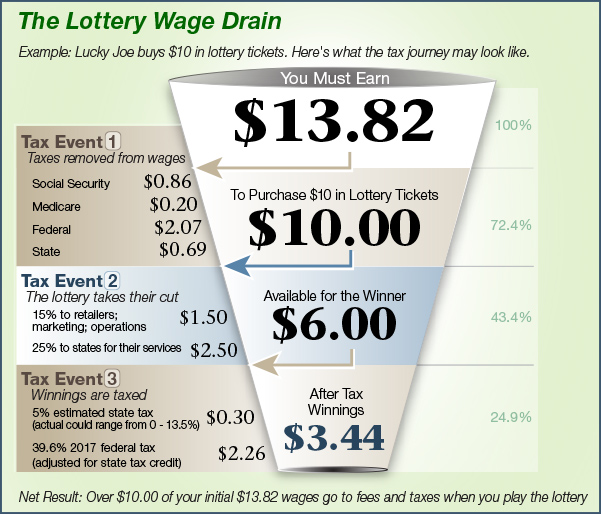

Many people dream of winning it big in the lottery. News media outlets publicize the large unclaimed pots of money on the evening news and they put a spotlight on the lucky multi-million dollar winners. Ever wonder what the tax math looks like?  The bottom line, when seen from a wage standpoint, is that 75% or more of the income used to play the lottery does not end up in the hands of the winner.

Only about a third of Americans file income tax returns using itemized deductions. Unfortunately many of those who don't itemize are overpaying their taxes. Don't wait until tax time to figure out if itemizing your deductions yields a lower tax bill. Start now to review your situation and plan for a reduction in your taxes by the end of the year.

The standard deduction for 2017 is $6,350 for individual taxpayers and $12,700 for married couples filing jointly. If you can identify deductions over these amounts, your taxable income will be lower. The first step in this process is to estimate your known itemized deductions. Start by breaking out your potential itemized deductions into these five piles. Pile #1: State and local taxes. You may deduct state and local taxes on either property or sales, but not both. If you live in a place with high property taxes, or you’ve made big purchases during the year and paid a lot in sales tax, this could be a big source of itemized deductions. Pile #2: Mortgage interest. You can deduct interest paid to secure a primary or secondary residence. Since interest payments are front-loaded onto the early years of a mortgage, this is a big deduction for new homeowners. Pile #3: Charitable contributions. Contributions to qualified charities can be used as itemized deductions. This includes cash donations, non-cash donations, and even mileage on behalf of qualified charities. Pile #4: Medical expenses. Medical expenses greater than 10 percent of your adjusted gross income can be deducted from an itemized tax return. Pile #5: Miscellaneous itemized deductions. With miscellaneous itemized deductions, you can generally deduct the total that exceeds 2 percent of your adjusted gross income. There are many potential deductions, such as:

Total up your potential deductions, remembering to only count the deductions for miscellaneous and medical expenses that exceed the adjusted gross income thresholds. If You're Close but Not Quite There If you are near your standard deduction threshold, here are some ideas to push you over the line.

On occasion, shifting deductions may result in using itemized deductions in one year and the standard deduction in the next. However, if you plan well, you'll have a lower total tax burden over the course of both years. Please feel free to ask for help if you would like to review your situation.  The number of Americans struggling with high debt is increasing, according to the US Federal Reserve. Household debt in the US reached a new record this spring, the central bank said, with the average indebted household owing more than $16,000 on their credit cards.

Seeking debt forgiveness from lenders is one option to try to deal with the burden of high debt. But there is an important tax consequence: Any amount of cancelled debt is generally taxed as ordinary income. This can come as a big surprise at tax time, when the relief of having settled a large debt is replaced by the anxiety of owing the IRS money. Common Debt Forgiveness Surprises Examples of when debt forgiveness can create a tax liability include:

Will Payoulater hadn’t been making payments on a $40,000 car loan and woke up one morning to find his driveway empty. The bank had repossessed the car and cancelled the remaining $35,000 balance on his loan. However, due to depreciation and wear-and-tear, the car’s market value was only $20,000 when it was repossessed. Not only is Will down one car, he’ll also have to pay taxes on the $15,000 difference as cancelled debt income. As you can see in this example, even the calculation of how much debt-forgiveness tax you owe can get complicated. What is the true market value of the car? Was the correct condition of the auto applied to the value? Getting some help from a tax professional can ensure you won't be overtaxed. Some Exceptions There are several situations where debt forgiveness is not taxable, including when:

If anyone you know is considering a debt settlement or has gone through one, please have them get in touch to work out the potential tax consequences.  If you have not already done so, now is the time to review your tax situation and make an estimated quarterly tax payment using Form 1040-ES. The second quarter due date is in just a few days.

Normal Due Date: Thursday, June 15, 2017 Remember, you are required to withhold at least 90% of your current tax obligation or 100% of last year’s federal tax obligation.* A quick look at last year’s tax return and a projection of this year’s obligation can help determine if a payment might be necessary. Here are some other things to consider:

With U.S. equity valuations near historically high levels, now may be an opportune time to take advantage of the tax benefits of donating long-term appreciated stock to a qualified charity. Directly donating a winning stock you've held for at least one year provides greater tax benefits than writing a check to your favorite cause.

Higher deduction. Your charitable gift deduction will be equal to the market value of the stock on the date of your donation, rather than what you originally paid for it. No capital gains tax. You avoid paying capital gains tax on the unrealized gains of the stock, because it is transferred directly to the charity rather than sold. That also means the charity gets a bigger gift. Example: John Diaz bought 50 Wonka Industries shares two years ago at $100.00 a share, and its shares have appreciated since then to $150.00 a share, giving him a long-term capital gain of $2,500 if he were to sell today. Instead, John avoids the capital gains tax by donating the shares to the Red Cross, and he deducts the full market value of $7,500 as an itemized deduction on his tax return. Some tips to keep in mind:

Wouldn't it be nice to have a source of nontaxable income? You may be more fortunate than you realize. Listed here are a number of income items that the IRS does not tax.

Remember when you pay for something in pre-tax dollars it's like giving yourself a raise. Because of this, be sure you take advantage of as many tax-free income opportunities as possible.  Getting audited isn't anyone's idea of a fun time, but you can minimize the stress if you take the right approach.

Step 1: Understand why and when. While it's possible you were selected randomly, it’s more likely you were selected for a specific reason. One example might be if your deductions for charitable donations or business expenses were greater than is typical for your income or profession. Before proceeding, make sure you understand what is being challenged and when you must reply. Your chance of being audited “randomly” rises along with the size of your income. With $200,000 a year in income your chance of being audited nearly doubles (1.01% in FY2016) compared with a person who has half of that income. People with more than $10 million in income have a nearly 1-in-5 chance of an audit every year. Step 2: Consider the type of audit. There are three kinds of audits, in increasing levels of seriousness: a correspondence audit, (conducted through the mail); an office audit (a visit to nearest IRS office); and a field audit (an IRS agent comes to visit you). How and what you prepare will vary depending on the type of audit. About 70 percent of audits are conducted through mail correspondence and they typically involve routine issues like providing information about deductions. With proper documentation and prompt attention, they can be relatively painless to resolve. Office and field audits can be trickier and will involve more work and preparation. Step 3: Gather documents. Once you’ve understood the reason and the type of audit, gather and organize as much of your relevant records as possible to prepare your response. For example, if the audit is specifically about deducting vehicle costs for business use, gather your mileage logbook, receipts and any other supporting documentation. This will help prove your case and let the IRS know you are a responsible taxpayer. If you do not have adequate documentation, you can try to get third-party corroboration. For example, if you took charitable deductions but lost the receipts, you could try reaching out to the charity for their records. While the charity cannot create “new” receipts, they may have copies of confirmations sent out to you at the time of your donation. Step 4: Know your rights. You have rights to ensure you get a fair chance to state your position. Specifically, you have the right to clear explanations about what the IRS wants and their decision regarding your case. You have the right to appeal the IRS’s decision. You also have the right to have your accountant or lawyer represent you during the audit. In addition, there is a special Taxpayer Advocate Service that is available to help you navigate through problems with your case. While you should stand up for your rights, always be polite with the IRS agent assigned to your case. They are just doing their job and you aren’t doing yourself any favors if you show hostility during your audit. Step 5: Get help. No matter what, reach out immediately if you get a letter from the IRS. It pays to have the right help, because an experienced professional can guide you away from costly mistakes. Too many taxpayers have corresponded with the IRS without this help and have paid the price. Try as you might, you probably do not know the tax law as well as the IRS. Audits happen. How you handle them can make all the difference.  As an employee, can you ever deduct the cost of a sporting event or other ticket on your expense report? Surprisingly, the answer can be yes, but only if you know and abide by the rules.

The Accountable Plan If your employer uses accountable plan rules for reimbursing expenses, the IRS will not only provide the ability for you to be reimbursed by your employer for your qualified expenses, it will also allow your employer to deduct the expense on their corporate tax return. To be a qualified expense, three rules must be met:

Applying the Rules To apply these expense deduction rules to a sporting event:

What Can Go Wrong? As you can imagine, the IRS looks closely at those who deduct entertainment as a qualified business expense. Here are some things to watch for:

As you make plans for the 2017 tax year, take note that three popular tax breaks expired last year and won't be available unless Congress acts to extend them.

Remember to plan for these changes. But also keep an eye on future action from Congress that could bring these dead tax deductions back to life. |

Archives

February 2018

Categories

All

|

RSS Feed

RSS Feed

|

Ellsworth & Associates, Inc. CPAs

513.272.8400 Cincinnati: 9624 Cincinnati Columbus Road, Suite 209, Cincinnati, OH 45241

|

© 2017 Ellsworth & Associates, Inc.

|