If you have not already done so, now is the time to review your tax situation and make an estimated quarterly tax payment using Form 1040-ES. The third-quarter due date is now here. Normal due date: Friday, September 15, 2017Remember you are required to withhold at least 90 percent of your current tax obligation or 100 percent of last year’s federal tax obligation.* A quick look at last year’s tax return and a projection of this year’s obligation can help determine if a payment is necessary. Here are some other things to consider:

Underpayment penalty. If you do not have proper tax withholdings, you could be subject to an underpayment penalty. The penalty can occur if you do not have proper withholdings throughout the year. So a payment at the end of the year may not help avoid the underpayment penalty. W-2 withholdings get special treatment. A W-2 withholding payment can be made at any time during the year and be treated as if it were made throughout the year. If you do not have enough to pay the estimated quarterly payment now, you may be able to adjust your W-2 withholdings to make up the difference. Self-employed. Remember to account for the need to pay your Social Security and Medicare taxes as well. Creating and funding a savings account for this purpose can help avoid the cash flow hit each quarter when you pay your estimated taxes. Don't forget state obligations. With the exception of a few states, you are often required to make estimated state tax payments when required to do so for your federal tax obligations. Consider conducting a review of your state obligations to ensure you meet these quarterly estimated tax payments as well. *If your income is over $150,000 ($75,000 if married filing separate), you must pay 110% of last year’s tax obligation to be safe from an underpayment penalty.

0 Comments

IRS scams are constantly changing, so you have to stay knowledgeable of the scammer's latest methods. Pretending to be an IRS agent is one of the favorite tactics of scam artists, according to the Better Business Bureau. The con artists impersonate the IRS to either intimidate people into making payments over the phone, or to send misleading emails tricking people into sharing personal information digitally. You can defend yourself against these scammers by knowing these simple rules: Rule #1: Expect a Letter FirstIn almost every case, the IRS will send you a letter via standard mail if they need to get in touch with you. This will alert you to expect future communication from the agency and instruct you on the best ways to get in touch with them. What to do: If you get a letter from the IRS that is unexpected or suspicious, it should have a form or notice number searchable on the IRS website. If something doesn't look right, you can call the IRS help desk at 1-800-829-1040 to question it. Rule 2: Never over EmailThe IRS will never initiate contact with you using email. A common scammer trick is to send emails to taxpayers using accounts and graphics that imitate the agency's. They may threaten imprisonment or fines if you don't pay up, or promise an extra refund if you send money to "prepay" your taxes. Often the emails contain links to an official-looking fake website to collect payments. Clicking on them may also trigger the installation of virus programs on your computer. What to do: Don't respond to any email communications supposedly from the IRS. Don't click on any links. Delete the email or forward it to phishing@irs.gov to help catch the scammers. Rule 3: Proper Phone Call EtiquetteAfter notification via the USPS, the real IRS may call you to discuss options to handle delinquent taxes or an audit. A real IRS agent or a debt collector won't demand immediate payment without giving you an opportunity to question or appeal the bill. Nor will they threaten lawsuits, arrest or deportation. Their tone should not be hostile or insulting. Finally, if they ask for payment, they should be asking you to make it out only to the United States Treasury. What to do: If you get a call from the IRS or an IRS debt collector, politely ask for the employee's name, badge number and phone number. They shouldn't hesitate to provide this information. You should then end the call and dial the IRS at 1-800-366-4484 to confirm the person's identity. Rule 4: Check In-Person VisitsAsk the person for their credentials. Every IRS agent should be able to produce two forms of credentials: a pocket commission card and a personal identity verification card issued by the Department of Homeland Security, also called an HSPD-12. What to do: Never provide sensitive information nor confirm information they may have without first independently verifying they are legitimate representatives of the IRS. If you have concerns you can call the IRS at 1-800-366-4484 to confirm the person's identity. You do not need to navigate this problem on your own. Call Ellsworth & Associates for assistance. It is good to have a knowledgeable expert on your side.

Recently the IRS certified 84 organizations as Certified Professional Employer Organizations (CPEO). This is the first group that was approved as part of the CPEO program. But what is a CPEO, and why does it matter?

Certified Professional Employer Organizations typically handle many payroll administration and tax reporting tasks for their business clients. Essentially, they hire the employees of their clients so that they can handle the taxes and payroll for those employees. This is called “co-employment”. In some cases, there have been abuses by PEOs. Usually this takes the form of the PEO withholding from an employee’s paycheck, but keeping that money for themselves. The IRS created the CPEO program in response to these abuses. In 2014, the IRS started a voluntary certification program for PEOs. After the IRS receives the required surety bond from an approved CPEO applicant, the IRS will publish that CPEO’s name, address, and effective date of certification on their website. Certification affects the employment tax liabilities of both the CPEO and its clients. A CPEO is normally treated as the employer of any individual performing services for a client of the CPEO and covered by a CPEO contract between the CPEO with the client, but only for wages and other compensation paid to the individual by the CPEO. To become and remain certified under the new program, CPEOs must meet tax compliance, background, experience, business location, financial reporting, bonding, and other requirements.  You can be audited within three years after the filing deadline of your tax return or when you actually filed your tax return. However, there are two main exceptions to this rule that can extend the risk of being audited:

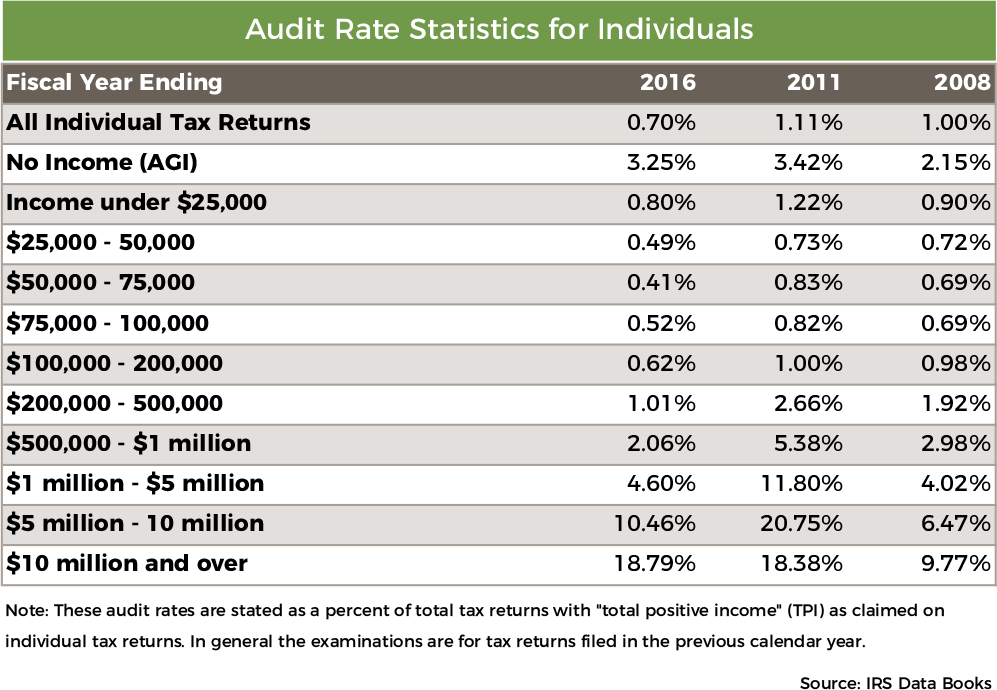

Every year the IRS publishes their examination statistics:  From 2008 to 2016 the overall audit rate for individual tax returns decreased from 1% to 0.7%. (For high income earners though, the audit rate has increased.)

The IRS is also auditing taxpayers with little to no taxable income. Much of this is due to the high incidence of error and fraud within the Earned Income Tax Credit. Play It Safe Always retain your tax records and support documents for as long as they may be needed to substantiate claims on your tax return. Make sure you consider any state record retention requirements as you review when it is safe to destroy old records. Remember some records need to be retained indefinitely. This includes, at minimum, copies of original tax returns, legal documents, and real estate transactions.  Wouldn't it be nice to have a source of nontaxable income? You may be more fortunate than you realize. Listed here are a number of income items that the IRS does not tax.

Remember when you pay for something in pre-tax dollars it's like giving yourself a raise. Because of this, be sure you take advantage of as many tax-free income opportunities as possible.  Getting audited isn't anyone's idea of a fun time, but you can minimize the stress if you take the right approach.

Step 1: Understand why and when. While it's possible you were selected randomly, it’s more likely you were selected for a specific reason. One example might be if your deductions for charitable donations or business expenses were greater than is typical for your income or profession. Before proceeding, make sure you understand what is being challenged and when you must reply. Your chance of being audited “randomly” rises along with the size of your income. With $200,000 a year in income your chance of being audited nearly doubles (1.01% in FY2016) compared with a person who has half of that income. People with more than $10 million in income have a nearly 1-in-5 chance of an audit every year. Step 2: Consider the type of audit. There are three kinds of audits, in increasing levels of seriousness: a correspondence audit, (conducted through the mail); an office audit (a visit to nearest IRS office); and a field audit (an IRS agent comes to visit you). How and what you prepare will vary depending on the type of audit. About 70 percent of audits are conducted through mail correspondence and they typically involve routine issues like providing information about deductions. With proper documentation and prompt attention, they can be relatively painless to resolve. Office and field audits can be trickier and will involve more work and preparation. Step 3: Gather documents. Once you’ve understood the reason and the type of audit, gather and organize as much of your relevant records as possible to prepare your response. For example, if the audit is specifically about deducting vehicle costs for business use, gather your mileage logbook, receipts and any other supporting documentation. This will help prove your case and let the IRS know you are a responsible taxpayer. If you do not have adequate documentation, you can try to get third-party corroboration. For example, if you took charitable deductions but lost the receipts, you could try reaching out to the charity for their records. While the charity cannot create “new” receipts, they may have copies of confirmations sent out to you at the time of your donation. Step 4: Know your rights. You have rights to ensure you get a fair chance to state your position. Specifically, you have the right to clear explanations about what the IRS wants and their decision regarding your case. You have the right to appeal the IRS’s decision. You also have the right to have your accountant or lawyer represent you during the audit. In addition, there is a special Taxpayer Advocate Service that is available to help you navigate through problems with your case. While you should stand up for your rights, always be polite with the IRS agent assigned to your case. They are just doing their job and you aren’t doing yourself any favors if you show hostility during your audit. Step 5: Get help. No matter what, reach out immediately if you get a letter from the IRS. It pays to have the right help, because an experienced professional can guide you away from costly mistakes. Too many taxpayers have corresponded with the IRS without this help and have paid the price. Try as you might, you probably do not know the tax law as well as the IRS. Audits happen. How you handle them can make all the difference.  Beginning this month, the IRS will begin sending letters to a relatively small number of taxpayers whose overdue federal tax accounts are being assigned to one of four private-sector collection agencies. The new program, authorized under a federal law enacted by Congress in December 2015, enables these designated contractors to collect unpaid tax debts on the government’s behalf. Usually, these are unpaid individual tax obligations that are not currently being worked by IRS collection employees and were assessed by the IRS several years ago. Taxpayers being assigned to a private firm would have had multiple contacts from the IRS in previous years and still have an unpaid tax bill. “The IRS is taking steps throughout this effort to ensure that the private collection firms work responsibly and respect taxpayer rights. The IRS also urges taxpayers to be on the lookout for scammers who might use this program as a cover to trick people. In reality, those taxpayers whose accounts are assigned as part of the private collection effort know they have a tax debt.”

—IRS Commissioner John Koskinen The program will begin this week with a few hundred taxpayers receiving mailings and subsequent phone calls, with the program increasing to thousands a week later in the spring and summer. Taxpayers with overdue taxes will always receive multiple contacts, letters and phone calls, first from the IRS, not private debt collectors.

The IRS will always notify a taxpayer before transferring their account to a private collection agency (PCA). First, the IRS will send a letter to the taxpayer and their tax representative informing them that their account is being assigned to a PCA and giving the name and contact information for the PCA. Four private debt collection agencies are participating in this program:

The IRS says a taxpayer’s account will only be assigned to one of these agencies, never to all four. No other private group is authorized to represent the IRS. Once the IRS letter is sent, the designated private firm will send its own letter to the taxpayer and their representative confirming the account transfer. To protect the taxpayer’s privacy and security, both the IRS letter and the collection firm’s letter will contain information that will help taxpayers identify the tax amount owed and assure taxpayers that future collection agency calls they may receive are legitimate. The private collectors will be able to identify themselves as contractors of the IRS collecting taxes. Employees of these collection agencies are supposed to follow the provisions of the Fair Debt Collection Practices Act, and reportedly told they, “must be courteous and must respect taxpayer rights.” The private firms are authorized to discuss payment options, including setting up payment agreements with taxpayers. But as with cases assigned to IRS employees, any tax payment must be made, either electronically or by check, to the IRS. A payment should never be sent to the private firm or anyone besides the IRS or the U.S. Treasury. Checks should only be made payable to the United States Treasury. Private firms are not authorized to take enforcement actions against taxpayers. Only IRS employees can take these actions, such as filing a notice of Federal Tax Lien or issuing a levy. Be on the lookout for scammers posing as private collection firms. Remember that these private collection firms will only be calling about a tax debt the person has had – and has been aware of – for years and had been contacted about previously by the IRS.  Nearly every taxpayer can imagine a worst-case scenario where they run afoul of the IRS and are selected for an audit. Here are a few areas that tend to get unwanted audit attention and ideas to help you stay prepared.

Your audit risk is (probably) low. The first thing to remember is that the risk of having your tax return examined by the IRS is probably very low. The IRS audits less than 1 in 100 returns. If you are among the roughly 95 percent of Americans who make less than $200,000 a year, your chance of being audited is closer to 1 in 200. Audit chances rise dramatically the higher your income is above $200,000, according to the IRS annual Data Book. Areas That Get Attention:

Thinking about calling the IRS this President's Day? There's good news and bad news. The good news is, because calls peak this time of year, and this day in particular, the IRS toll-free lines will be open Monday, Feb. 20, from 7 a.m. to 7 p.m. The bad news is, they are at their busiest, so be prepared to wait on hold longer than usual. If your question can wait, don't call today.

If you need to call the IRS this tax season, be prepared to validate your identity when speaking with an IRS representative. This will help avoid the need for a repeat call. IRS phone representatives will only discuss personal information with the taxpayer or someone authorized to speak on their behalf. If you're calling about your personal tax account, have the following information handy:

If you're calling to check on the status of your refund, a better option is to use the "Where's My Refund?" tool. For information on a state return, a good starting point is our Tax Refund Status page. |

Archives

February 2018

Categories

All

|

RSS Feed

RSS Feed

|

Ellsworth & Associates, Inc. CPAs

513.272.8400 Cincinnati: 9624 Cincinnati Columbus Road, Suite 209, Cincinnati, OH 45241

|

© 2017 Ellsworth & Associates, Inc.

|